ADVANCED ENERGY ECONOMY INSTITUTE

Executive Summary

Questions have been raised about whether renewable energy (RE) and energy efficiency (EE) resources can provide substantial emission reductions at reasonable cost under EPA’s proposed Clean Power Plan (CPP). These concerns reflect fundamental misperceptions about the performance and cost of today’s renewable energy and energy efficiency technologies, rooted in outdated information and perpetuated by inaccurate official market projections. This paper shows that RE and EE are competitive resources in today’s marketplace that will not only be cost-effective mechanisms for CPP compliance but should also be expected to grow strictly on the basis of competitiveness.

EIA Forecasts Consistently Underestimate RE and EE Compared to Market Realities

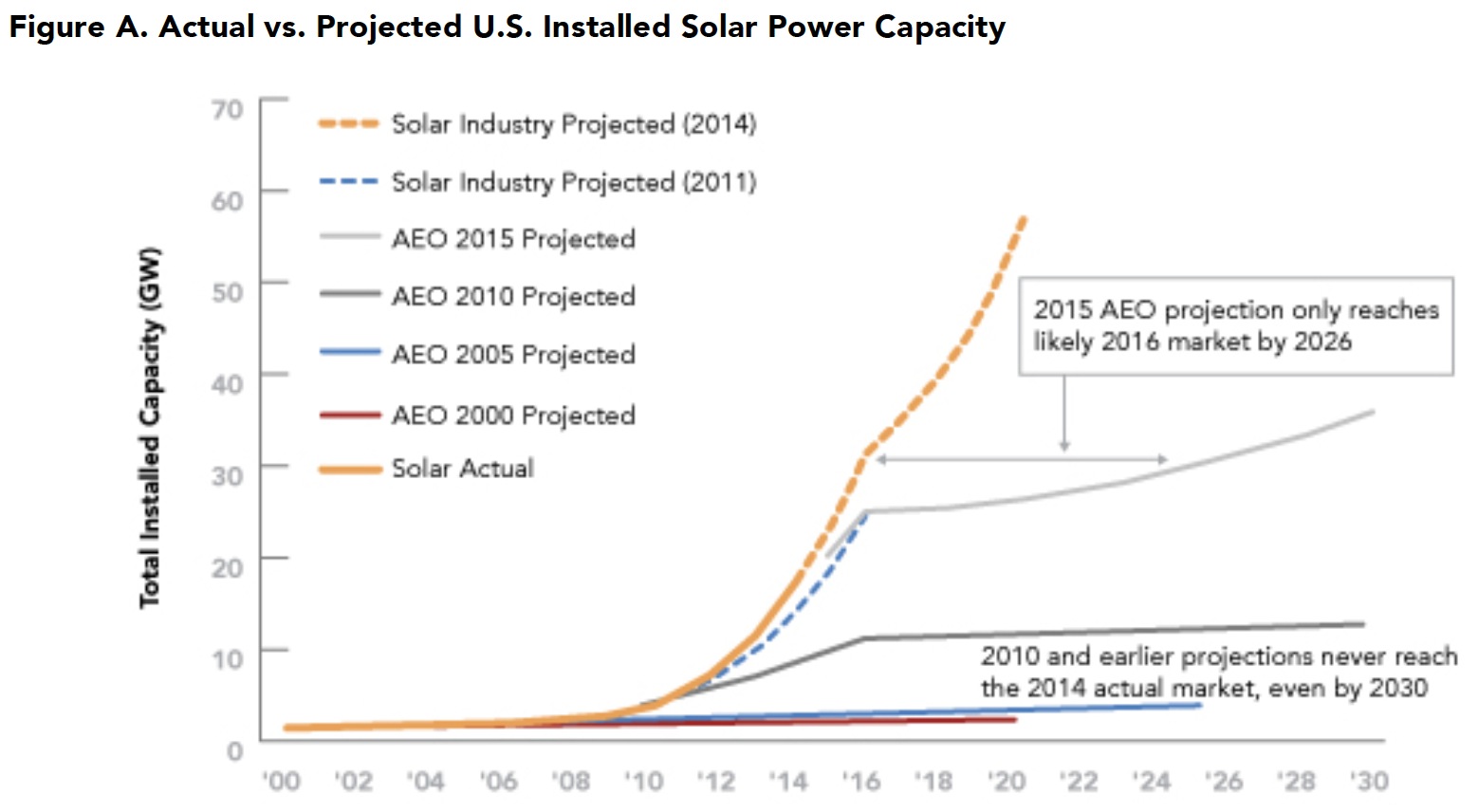

Official U.S. government energy forecasts are widely used by policymakers and other stakeholders for analyzing energy supply and demand for long-term planning and policy development purposes. But the RE projections bear little resemblance to market realities. The U.S. Energy Information Administration’s Annual Energy Outlook (AEO), the primary source of information on U.S. power market projections, consistently and significantly underestimates RE growth. For example, the installed generating capacity of solar power is likely to double between 2014 and 2016, based on market analyses that take into account actual projects in the pipeline. Yet in the AEO 2015 forecast, solar capacity does not double until 2026. Similarly, U.S. wind installations have averaged about 6.5 GW per year from 2007 to 2014, but the 2015 AEO projects a total of 6.5 GW of new wind capacity will be added between 2017 and 2030, less than one-tenth the average rate in recent years.

This underestimation of RE growth is nothing new. AEO 2010 projected that the solar market would grow from about 2.5 GW in 2010 to about 13 GW in 2030, yet the solar market surpassed this level in 2014. Similarly, AEO 2010 projected that the wind market would grow from about 40 GW in 2010 to 69 GW by 2030, but with 8-10 GW of new wind power expected in 2015, installed capacity will reach about 75 GW by year’s end. As these examples show, AEO forecasts are consistently off by a wide margin, always underestimating – and never overestimating – future deployment of renewables. Such persistent inaccuracy is indicative of a more fundamental problem in understanding the dynamics of growth for these technologies, as well as constraints on how the EIA is required to conduct its modeling.

Comparing market realities to projections for energy efficiency is more challenging. To quantify EE, you need to measure something that was avoided, namely the energy that would have been used absent the energy efficiency measures. Still, official projections are inconsistent with trends in EE implementation and the impact of efficiency improvements on electricity consumption. The trend in overall electric demand growth has been consistently downward in recent years, in parallel with the rise in EE spending, which more than tripled from 2005 to 2013. Retail electricity sales have also been flat to slightly declining since 2010, even as the economic recovery gained momentum and the U.S. economy grew about 9% in real terms from 2010 to 2014. Yet the AEO 2015 projection shows future demand growth steady at a little less than 1% per year out to 2040, apparently discounting the potential, or likelihood, that EE improvement – through investment and innovation – would continue to reduce demand growth in the coming years.

Renewable Energy is Increasingly Cost Competitive with Other Power Sources

There is every reason to believe that renewable energy will continue to grow in the United States based on economic competitiveness. The most basic indicator of power technology competitiveness is the levelized cost of energy (LCOE), which measures the average cost of electricity over the life of a project, including the costs of upfront capital, operations and maintenance, fuel, and financing. Since 2007, Lazard, a financial advisory and asset management firm, has tracked the LCOE of power technologies using a consistent methodology. Lazard’s annual analyses show that from 2009 to 2014, the LCOE for utility-scale wind and solar power has declined by 58% and 78%, respectively, such that RE technologies are increasingly competitive with other power sources.

Market data in the form of power purchase agreement (PPA) prices confirm these LCOE estimates, with wind projects offering competitive PPA prices relative to wholesale prices for most of the past decade. In 2013, the average wind power PPA price was $24/MWh. Similarly, solar PPAs, which provide utilities with peaking power, have declined from $125-$150/MWh in 2008 to current levels of $50-$75/MWh, driven in part by a 40% drop in the installed cost of utility-scale PV systems over five years, from $5/WDC in 2008 to $3/WDC in 2013. Today, the best-in-class utility-scale solar projects are being installed for about $1.50/WDC, which is about half the cost assumed by the EIA in its AEO 2015 for a 2016 year-in-service date. Hydropower, geothermal and biomass technologies are also competitive in some parts of the country. Although their markets are smaller than solar or wind, capacity continues to be added at a rate of several hundred megawatts per year among them.

Utility RE purchases that were once driven primarily by state policies (e.g., renewable portfolio standards) are now increasingly made based on economics. In Texas, Austin Energy signed a 20-year contract in 2014 for 150 MW of solar energy at a price estimated at less than $50/MWh. In 2013, American Electric Power (AEP) bought three times more wind power in Oklahoma than it originally intended because of its value to ratepayers. None of this is lost on corporate America, which is directly purchasing a growing share of RE. In 2014, more than 23% of wind power contracts were with large corporate or non-utility groups.

The market for residential and commercial building PV systems, usually installed on rooftops, is also expanding in response to declining costs, rising retail electricity rates, new financing options, and increased customer demand for choice and control over energy use and costs. Prices for residential and small commercial PV systems dropped by almost 60% between 2002 and 2013, with most of that occurring since 2009. As the solar iii Renewable Energy and Energy Efficiency Competitiveness supply chain achieves scale (about 2 GW of distributed PV was installed in the United States in 2014), the industry is driving down so-called “soft costs” such as permitting, customer acquisition, and installation.

Download full version (PDF): Competitiveness of Renewable Energy & Energy Efficiency in U.S. Markets

About the Advanced Energy Economy Institute

www.aee.net

The Advanced Energy Economy Institute (AEE Institute) is a 501(c)(3) charitable organization whose mission is to raise awareness of the public benefits and opportunities of advanced energy. AEE Institute provides critical data to drive the policy discussion on key issues through commissioned research and reports, data aggregation, and analytic tools. AEE Institute also provides a forum where leaders can address energy challenges and opportunities facing the United States. AEE Institute is affiliated with Advanced Energy Economy (AEE), a 501(c)(6) business association, whose purpose is to advance and promote the common business interests of its members and the advanced energy industry as a whole.

Tags: Advanced Energy Economy Institute, AEE, PV, Renewable Energy

RSS Feed

RSS Feed